ดาวน์โหลดงานนำเสนอ

งานนำเสนอกำลังจะดาวน์โหลด โปรดรอ

1

www.14iacc.org www.iacconference.org www.twitter.com/14iacc

Governance and Power Development Planning in Thailand Suphakit Nuntavorakarn Healthy Public Policy Foundation and National Independent Commission on Environment and Health (Provisional) 13 November 2010

13 November")

2

Power Development Plan (PDP) and its importance

PDP is the long-term strategic plan of the Thai power sector (15-20 years timeframe) PDP determines the future investment - how many and which types of power plant? For example, total investment of PDP billion USD PDP also determines the future impacts of the power sector, including environmental, economic, social, and health impacts

PDP determines the future investment - how many and which types of power plant For example, total investment of PDP billion USD. PDP also determines the future impacts of the power sector, including environmental, economic, social, and health impacts.")

3

Electricity Governance in Thailand, 2nd Assessment (2006-2008)

Aim toward constructive engagement to encourage good governance Develop and communicate the concept and assessment direction to the stakeholders since the beginning period Participate and observe the relevant meetings and forums, as well as arrange the public forum on Power Planning for local communities and energy networks Through the multi-stakeholders Advisory Committee, develop the indicators as well as review the draft report

4

Comprise of four parts, 14 indicators

Electricity Governance Assessment (2nd Assessment) The part on Power Development Planning2007 Apply the indicators from EGT and review the draft report by multi-stakeholders advisory committee Comprise of four parts, 14 indicators Transparency and access to information Participation Capacity Accountability and redress mechanism

The part on Power Development Planning2007. Apply the indicators from EGT and review the draft report by multi-stakeholders advisory committee. Comprise of four parts, 14 indicators. Transparency and access to information. Participation. Capacity. Accountability and redress mechanism.")

5

Electricity Governance Assessment on PDP2007

Many governance problems in the PDP2007, reflecting from many indicators in all four parts Leading to questions for the approval of the PDP2007 and then, problems in the implementation, for example much higher fuel price than the assumptions in the PDP conflicts and protests in all four IPP projects and none can proceed to construction until the present

6

The key recommendation from EGT on PDP

7

The policy for Power Development Planning 2010

On 7th October 2009, Ministry of Energy announced the ‘Green PDP’ policy for PDP2010 Systematic public participation process Reduce GHG emission from PDP2007 Introducing ‘End-Use’ approach for demand forecast Following the targets in the Renewable Energy Development Plan by Ministry of Energy Open for different PDP options and performing Impact Assessment to compare these options

8

Governance problems of the recent Power Development Plan 2010-2030

MoE made the first draft of PDP2010 since January 2010 without any public inputs or participation MoE made decision not to use the ‘End-Use Approach’ study, commissioned by themselves

9

Governance problems of the recent Power Development Plan 2010-2030

The first public hearing on draft PDP2010 on 17th Feb., while the ‘Long-term GDP Growth’ study, commissioned by MoE is not finished yet. The second public hearing on 8th Mar. on draft PDP2010, only four days after a technical hearing on the ‘Long-term GDP Growth’ study

10

Governance problems of the recent Power Development Plan 2010-2030

The Senate Sub-Committee on PDP arranged two public forums on 4th and 11th March, with representative of MoE said that ‘they will postpone the submission for approval’ due to the ‘Red Shirt’ protest and demonstration The National Energy Policy Council approved PDP2010 on 12th March and the government approved on 23rd March, during severe political conflicts in the society

11

Installed Capacity at the end of 2030

Unit : MW - Nuclear 1000 MW 5,000 (5โรง) - CCGT 16,670 (19โรง) - Imported coal 8,400 (13โรง) SPP Co-Gen. 6,919 Renewables (VSPP, EGAT) 5,348 - Import from neighboring countries 11,669 Installed Capacity at the end of ,213 New Installed Capacity 54,005 Decommission - 17,671 Installed Capacity at the end of ,547 PDP2010 GDP Base case New power plants กำลังผลิตไฟฟ้า

- CCGT 16,670 (19โรง) - Imported coal 8,400 (13โรง) SPP Co-Gen. 6,919. Renewables (VSPP, EGAT) 5, Import from neighboring countries 11,669. Installed Capacity at the end of ,213. New Installed Capacity 54,005. Decommission - 17,671. Installed Capacity at the end of ,547. PDP2010 GDP Base case. New power plants กำลังผลิตไฟฟ้า.")

12

PDP2010 (GDP Base case) Installed Capacity by fuel type

เมกะวัตต์ ปี 45% 49% 54% 61% 64% 68% 65% 66% 67% 63% 60% 57% 51% 47% 44% 43% 42% 5% 7% 8% 9% 12% 11% 13% 15% 17% 6% 4% 10% 14% 16% 18% PDP2010 : (GDP กรณีฐาน) Renewables Import Gas Imported coal Nuclear

Renewables. Import. Gas. Imported coal. Nuclear.")

13

An Alternative PDP Needed new capacity - Peak demand 52,890 MW in 2030

- Reserve Margin at 15% would need 60,824 MW in 2030 - Not 65,547 MW in 2030 as determined in PDP2010 - Need better arrangement of all Installed Capacity

14

Save 0.3% of the peak demand in 20 years

DSM in PDP2010 Saving target of T5 high efficiency light bulb program ปี 2010 2011 2012 2013 2014 2015 2016 2017 2018 MW 43 129 215 344 473 584 498 369 198 Save 0.3% of the peak demand in 20 years ปี 2553 2554 2555 2556 2557 2558 2559 2560 2561 MW 43 172 387 731 1,204 1,788 2,286 2,655 2,853 Saving target of DSM program for ปี 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028 2029 2030 MW 240 ปี 2562 2563 2564 2565 2566 2567 2568 2569 2570 2571 2572 2573 MW 3,093 3,333 3,573 3,813 4,053 4,293 4,533 4,773 5,013 5,253 5,493 5,733 14

15

Average saving of 1,170 GWh/year

DSM in PDP2010 DSM in PDP2010 Press meeting by MoE “T5 high efficiency light bulb program will save around 8,708 GWh per year or reduce the expenses of 26,124 million Baht per year” Average saving of 1,170 GWh/year Ref. : EPPO 17th Feb Ref. : EPPO 29/09/

16

Save 12% in 10 years and 29% in 20 ปี

17

DSM&EE Potential in the Industrial Sector

Financially viable potential, around 42% of total demand in the Industrial Sector (Tira Foran, 2010) Consider achievable savings and achievable facilities Market potential in 10 year Save 10% of total demand in the sector Around 10,498 GWh , 1,680 MW

Consider achievable savings and achievable facilities. Market potential in 10 year. Save 10% of total demand in the sector. Around 10,498 GWh , 1,680 MW.")

18

An Alternative PDP Renewable Energy - Follow the High Renewables scenario of the draft PDP Target of 8,581 MW in Adjust the growth to achieve the goal of 5,608 MW in the Renewable Energy Development Plan by MoE

19

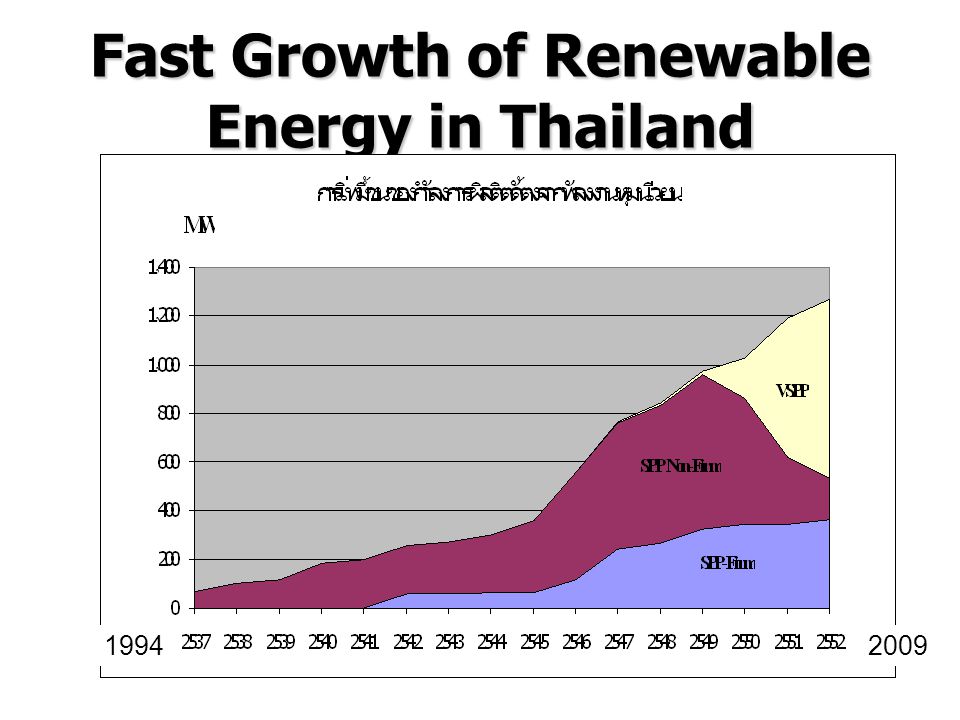

Fast Growth of Renewable Energy in Thailand

1994 2009

20

Numbers of Renewable Energy Projects applying for Investment Promotion

Number of Projects Total Investment (billion Baht) 2008 62 19.9 2009 402 229.0

")

21

An Alternative PDP Co-generation and Tri-generation, that have much higher energy efficiency, when compared to conventional power plants - Follow the target in the draft PDP2010 8,631 MW in But will rebuild the existing projects, which will be retired during ,798 MW Repowering, or building new power plant at the site of retired plant 13,600 MW

22

An Alternative PDP รายการ เมกะวัตต์ New Installed Capacity 2010-2030

54,625 Better arrangement of all Installed Capacity 5,344 Demand Side Management (15% of the Peak Demand) 8,136 Renewable energy 8,581 Co-generation and Tri-generation 10,429 Repowering 13,600 Can decrease the new installed capacity 46,090 New Power Plant Projects needed for 8,535

8,136. Renewable energy. 8,581. Co-generation and Tri-generation. 10,429. Repowering. 13,600. Can decrease the new installed capacity. 46,090. New Power Plant Projects needed for ,535.")

23

Strategic Impact Assessment on different PDP options

Impact on energy security Import burden and GDP contribution GHG emission Air pollution and waste Health impacts Job creation Should be share and discuss through public deliberation process

24

DSM/EE is the cheapest energy option,

but PDP2010 chose the expensive ones and try to make them look cheap, like coal and nuclear Comparison of electricity cost from different options in Pacific Northwest, USA. Resource potential for generic coal, gas & wind resources shown for typical unit size. Additional potential is available at comparable costs. Source: Northwest Power and Conservation Council 24

25

Investment and fuel costs in PDP 2010

โรงไฟฟ้า กำลังผลิต เงินลงทุน (ปี 2552) Heat Rate อายุ การใช้งาน ราคาเชื้อเพลิง (ปี 2563) ต้นทุน (บาท/kWh) (เมกกะวัตต์) ($/kW) (Btu/kWh) (ปี) ($/MMbtu) AP EP รวม โรงไฟฟ้าถ่านหิน 800 1,550 9,125 30 4.01 1.27 1.37 2.64 โรงไฟฟ้านิวเคลียร์ 1000 3,087 10,953 60 0.50 2.60 0.19 2.79 โรงไฟฟ้าถ่านหิน (CCS) 2,632 1.99 3.36 โรงไฟฟ้าพลังความร้อนร่วม (Gas Existing) 727 6,800 25 11.12 0.65 3.04 3.69 โรงไฟฟ้าพลังความร้อนร่วม (Marginal Gas) 14.26 4.34 โรงไฟฟ้ากังหันแก๊ส 290 437 10,410 20 30.66 2.05 11.69 13.74 CPI ปีละ 3.5%, MUV ปีละ 0.5% อัตราเพิ่ม O&M ปีละ 3.5% หมายเหตุ โรงไฟฟ้านิวเคลียร์ ราคารวม - Power Plant Equipment - Site Preparation & Civil Work - Raw Water System - Land & Land Right - ระบบเก็บรักษาและกำจัดกากเชื้อเพลิง - อื่นๆ โรงไฟฟ้าถ่านหิน - ใช้เทคโนโลยี Supercritical หรือ Ultra Supercritical - ใช้ถ่านหินนำเข้าประเภท Bituminous - ติดตั้งระบบ FGD 25

Heat Rate. อายุ การใช้งาน. ราคาเชื้อเพลิง. (ปี 2563) ต้นทุน (บาท/kWh) (เมกกะวัตต์) ($/kW) (Btu/kWh) (ปี) ($/MMbtu) AP. EP. รวม. โรงไฟฟ้าถ่านหิน ,550. 9, โรงไฟฟ้านิวเคลียร์ , , โรงไฟฟ้าถ่านหิน (CCS) 2, โรงไฟฟ้าพลังความร้อนร่วม (Gas Existing) , โรงไฟฟ้าพลังความร้อนร่วม (Marginal Gas) โรงไฟฟ้ากังหันแก๊ส , CPI ปีละ 3.5%, MUV ปีละ 0.5% อัตราเพิ่ม O&M ปีละ 3.5% หมายเหตุ โรงไฟฟ้านิวเคลียร์ ราคารวม. - Power Plant Equipment. - Site Preparation & Civil Work. - Raw Water System. - Land & Land Right. - ระบบเก็บรักษาและกำจัดกากเชื้อเพลิง. - อื่นๆ. โรงไฟฟ้าถ่านหิน. - ใช้เทคโนโลยี Supercritical หรือ Ultra Supercritical. - ใช้ถ่านหินนำเข้าประเภท Bituminous. - ติดตั้งระบบ FGD. 25.")

26

Prices in the last 10 years (US$/MMBTU)

Fuel prices in PDP2010 Prices in the last 10 years (US$/MMBTU) ที่มา:

ที่มา: commodity=coal-australian&months= commodity=crude-oil-dubai&months=300.")

27

The problematic regulation and conflicts of interests

28

ROIC and Investment Efficiency

Using Return on Invested Capital (ROIC) as the main criteria for setting electricity tariff may lead to over investment since more investment means more profit Strong regulation on investment plans is needed, but the Regulators still lack of data, knowledge, and human resources to check and balance The approval of the tariff is still with the National Energy Policy Council ROIC = Net profit after tax Investment EGAT 8.4% MEA PEA 4.8% Result : Over Demand Forecast and prefer high investment options

as the main criteria for setting electricity tariff may lead to over investment. since more investment means more profit. Strong regulation on investment plans is needed, but the Regulators still lack of data, knowledge, and human resources to check and balance. The approval of the tariff is still with the National Energy Policy Council. ROIC = Net profit after tax. Investment. EGAT 8.4% MEA. PEA. 4.8% Result : Over Demand Forecast and prefer high investment options.")

29

The cycle of supporting more investment under ‘monopoly’ power

Over Demand Forecast Power Planning that prefer high investment options 1 Benefits of utilities, energy companies, etc. 2 3 Electricity tariff that allow the pass on of excess costs to consumers

30

Ft : Fuel Adjustment Charge

EGAT: a part of the electricity tariff that increase or decrease automatically, according to changes in fuel costs and other uncontrol costs The mechanism to pass on the costs to consumers, which includes Fuel costs Electricity price for private producers and import (including profit guarantee, compensation for inflation and exchange rate) Expenses according to government policies (e.g. Community Development Funds, ‘Adder’ for renewable energy, etc.) Compensation for lower sale (or over investment)

Expenses according to government policies (e.g. Community Development Funds, ‘Adder’ for renewable energy, etc.) Compensation for lower sale (or over investment)")

31

Power Business PTT MEA EGAT Banpu BLCP CLP Glow Energy ราชบุรี

35% MEA 35% EGAT CLP Glow Energy Banpu 30% 45% 14.99% 25.41% 22.42% Gluf Electric บริษัท กัลฟ์ อิเลคทริค จำกัด Thai Oil Plc. บริษัท ไทยออยล์ จำกัด 15% RATCH บริษัท ราชบุรี โฮลดิ้ง จำกัด EGCO บริษัท ผลิตไฟฟ้า จำกัด 50% 50% 54.99% ราชบุรี อัลลัยแอนซ์ 50% 26% Thai Oil Power บริษัท ไทยออยล์ จำกัด 56% 24% 25% 100% 50% 100% 100% 100% 100% ผลิตไฟฟ้า อิสระ 700 MW ผลิตไฟฟ้า และน้ำเย็น ราชบุรี เพาเวอร์ 1,400 MW ผลิตไฟฟ้า ราชบุรี 3,645 MW ไตร เอนเนอยี 700 MW ระยอง 1,232 MW ขนอม 824 MW แก่งคอย 1,468 MW Glow IPP 713 MW บริษัท โกลว์ ไอพีพี จำกัด BLCP 1,468 MW 15% 14.85% 80% 70.3% 100% 100% 100% 100% อมตะ เพาเวอร์ บางปะกง 112 MW อมตะ เอ็กโก เพาเวอร์ 165 MW ทีแอลพี โคเจน 117 MW ร้อยเอ็ด กรีน 9.9 MW กัลฟ์ โคเจนเนอเรชั่น 110 MW หนองแค โคเจนเนอเรชั่น 126 MW สมุทรปราการ โคเจนเนอเรชั่น 126 MW กัลฟ์ ยะลา 23 MW โกลว์ พลังงาน 358 MW โกลว์ เอสพีพี1 124 MW โกลว์เอสพีพี2/ โกลว์เอสพีพี3 514 MW 31

32

Conflict of Interests in Ministry of Energy

The exception in the National Energy Policy Council Act B.E.2551 (2008) Section 5/1. A Member of the National Energy Policy Council shall: (2) not hold any post in a juristic entity operating a business related to the generation, transmission or distribution of non-renewable energy or electricity, except for the case that the Member of the National Energy Policy Council is a civil servant, who has been assigned by the government or by the Board of a given state-owned enterprise to assume a post of Board Member or any other post in that state-owned enterprise operating an energy-related business or in a juristic entity of which the state-owned enterprise is a shareholder.

Section 5/1. A Member of the National Energy Policy Council shall: (2) not hold any post in a juristic entity operating a business related to the generation, transmission or distribution of non-renewable energy or electricity, except for the case that the Member of the National Energy Policy Council is a civil servant, who has been assigned by the government or by the Board of a given state-owned enterprise to assume a post of Board Member or any other post in that state-owned enterprise operating an energy-related business or in a juristic entity of which the state-owned enterprise is a shareholder.")

33

Conflict of Interests in Ministry of Energy

The exception in the Standard Characteristic for Board and Staff of State-owned Enterprise B.E.2550 (2008) Section 6 Board member in State-owned Enterprise shall: (10) not hold any post in a juristic entity that get the concession, joint venture, or has the link to the State-owned Enterprise, except for the case that has been assigned by the State-owned Enterprise to be Chair of the board, board member, or executive staffs

Section 6 Board member in State-owned Enterprise shall: (10) not hold any post in a juristic entity that get the concession, joint venture, or has the link to the State-owned Enterprise, except for the case that has been assigned by the State-owned Enterprise to be Chair of the board, board member, or executive staffs.")

34

Role in the private sector

Examples (Data in 2008) Role in the Government Role in the private sector Mr.Pornchai Rujiprapa Secretary-General, Ministry of Energy Chair of the Board, Electricity Generating Authority of Thailand National Energy Policy Council Board, Electricity Generating Company (EGCO) (resign in 2007) Chair, Sub-Committee on Electricity Demand Forecast Chair of the Board, PTT (resign in 2007) Chair, Committee on PDP Revision Chair of the Board, PTT Chemical, PTT Aromatics and Refineries Chair, Committee of Energy Fund Administrative Institute Chair of the Board,

Role in the Government. Role in the private sector. Mr.Pornchai Rujiprapa. Secretary-General, Ministry of Energy. Chair of the Board, Electricity Generating Authority of Thailand. National Energy Policy Council. Board, Electricity Generating Company (EGCO) (resign in 2007) Chair, Sub-Committee on Electricity Demand Forecast. Chair of the Board, PTT (resign in 2007) Chair, Committee on PDP Revision. Chair of the Board, PTT Chemical, PTT Aromatics and Refineries. Chair, Committee of Energy Fund Administrative Institute. Chair of the Board,")

35

Example Annual benefits to Chair of the Board, PTT in 2008

Mr.Norkhun Sittipong, Deputy Secretary-General, Ministry of Energy Baht Role in the private sector Meeting Allowance Bonus Total Chair of the Board 770,000 2,200,000 2,900,000 Role in the Government sector Salary Addition for Executive position Total Deputy Secretary-General, Ministry of Energy 804,000 252,000 1,056,000 35

36

National Energy Policy Council, Chaired by PM

Energy Policy Administrative Committee, Chaired by Energy Minister Sub-committee on EGAT Coordination Sub-committee on Waste-to-Energy Secretary-General or the Deputy Secretary-Generals is the chair of the Sub-committees Sub-committee on Energy Eff. Std. Sub-committee on Demand Forecast Sub-committee on Hydropower Sub-committee on PDP Sub-committee on DSM Energy Policy and Planning Office, MoE is secretariat of the Sub-committees Sub-committee on Environment and Energy Sub-committee on an IPP project Sub-committee on Renewable Energy Sub-committee on Community Development Funds 36

37

Recommendations to improve the PDP process

Change the ROIC to Performance-based regulation Introduce Contracted Demand to large electricity users (e.g. more than 10 MW) Improve the Ft by excluding the compensation for lower sale DSM should be considered as one investment option for electricity supply Compare various draft PDPs, according to Government policies and planning objectives Integrated Resource Planning; IRP Various forums, dialogue, etc. for public deliberation

Improve the Ft by excluding the compensation for lower sale. DSM should be considered as one investment option for electricity supply. Compare various draft PDPs, according to Government policies and planning objectives. Integrated Resource Planning; IRP. Various forums, dialogue, etc. for public deliberation.")

38

Toward Reflexive Governance in the PDP process

39

Thank you for your attention

งานนำเสนอที่คล้ายกัน

(ต่อ)>")

และแนวโน้มไตรมาส 3/50 และ 4/50>")