ดาวน์โหลดงานนำเสนอ

งานนำเสนอกำลังจะดาวน์โหลด โปรดรอ

1

วัฎจักรทางการบัญชี –ภาคจบ (THE ACCOUNTING CYCLE 2)

Chapter 5 2

2

At the end of the period, we need to make adjusting entries to get the accounts up to date for the financial statements.

3

Adjusting Entries Adjusting entries are Every adjusting

needed whenever revenue or expenses affect more than one entry involves a change in either a revenue or expense accounting period. and an asset or liability. 4

4

Types of Adjusting Entries

1. Accruing uncollected revenues: รายได้ค้างรับ 4.Converting assets to expenses: ค่าใช้จ่ายจ่ายล่วงหน้า 2.Accruing unpaid expenses:ค่าใช้จ่ายค้างจ่าย 5.Doubtful account: หนี้สงสัยจะสูญ 6.Depreciation:ค่าเสื่อมราคา 3.Converting liabilities to revenue:รายได้รับล่วงหน้า

5

1.Accruing Uncollected Revenue

End of Current Period Prior Periods Current Period Future Periods Adjusting Entry Recognizes revenue earned but not yet recorded, and Records receivable. Transaction Receivable will be collected. 4

6

1.Accruing Uncollected Revenue

Examples Include: Interest Earned Work Completed But Not Yet Billed to Customer 4

7

1.Accruing Uncollected Revenue

$170 Interest Revenue Saturday, Jan. 15 Monday, Jan. 31 Tuesday, Feb. 15 On Jan. 31, the bank owes Webb Co. interest of $ Interest is paid on the 15th day of each month. 4

8

1.Accruing Uncollected Revenue

Initially, the revenue is recognized and a receivable is created. 4

9

1.Accruing Uncollected Revenue

Balance Sheet Receivable to be collected in a future period. Income Statement Revenue earned this period. 4

10

1.Accruing Uncollected Revenue

$320 Monthly Interest $170 Interest Revenue $150 Interest Revenue Saturday, Jan. 15 Monday, Jan. 31 Tuesday, Feb. 15 Let’s look at the entry for February 15. 4

11

1.Accruing Uncollected Revenue

The receivable is collected in a future period. 4

12

2.Accruing Unpaid Expenses

End of Current Period Prior Periods Current Period Future Periods Adjusting Entry Recognizes expenses incurred, and Records liability for future payment. Transaction Liability will be paid. 4

13

2.Accruing Unpaid Expenses

Hey, when do we get paid? Examples Include: Interest Wages and Salaries Property Taxes 4

14

2.Accruing Unpaid Expenses

$3,000 Wages Expense Monday, May 29 Wednesday, May 31 Friday, June 2 On May 31, Webb Co. owes wages of $3,000. Pay day is Friday, June 2. 4

15

2.Accruing Unpaid Expenses

Initially, an expense and a liability are recorded. 4

16

2.Accruing Unpaid Expenses

Balance Sheet Liability to be paid in a future period. Income Statement Cost incurred this period to generate revenue. 4

17

2.Accruing Unpaid Expenses

$5,000 Weekly Wages $3,000 Wages Expense $2,000 Wages Expense Monday, May 29 Wednesday, May 31 Friday, June 2 Let’s look at the entry for June 2. 4

18

2.Accruing Unpaid Expenses

The liability is extinguished when the debt is paid. 4

19

3.Converting Liabilities to Revenue

End of Current Period Prior Periods Current Period Future Periods Transaction Collected from customers in advance (creates a liability). Adjusting Entry Recognizes portion earned as revenue, and Reduces balance of liability account. 4

. Adjusting Entry. Recognizes portion. earned as revenue, and. Reduces balance of liability account. 4.")

20

3.Converting Liabilities to Revenue

Examples Include: Airline Ticket Sales Sports Teams’ Sales of Season Tickets 4

21

3.Converting Liabilities to Revenue

$6,000 Rental Contract Coverage for 12 Months $500 Monthly Rental Revenue Jan. 1 Dec. 31 On January 1, Webb Co. received $6,000 in advance for a one-year rental contract. 4

22

3.Converting Liabilities to Revenue

ตอนรับเงินรายได้ บันทึกบัญชีได้ 2 วิธี 1.บันทึกเป็นรายได้ทั้งจำนวน 2.บันทึกไว้เป็นหนี้สิน(รายได้รับล่วงหน้า) เมื่อสิ้นงวดการปรับปรุงจะแตกต่างกันระหว่าง 2 วิธี แต่ผลลัพธ์จะเท่ากัน

เมื่อสิ้นงวดการปรับปรุงจะแตกต่างกันระหว่าง 2 วิธี แต่ผลลัพธ์จะเท่ากัน.")

23

3.Converting Liabilities to Revenue

1.บันทึกเป็นรายได้ทั้งจำนวน 1.1 ตอนรับเงิน: Dr. เงินสด xx Cr. รายได้ xx 1.2 ปรับปรุงตอนสิ้นงวด: Dr. รายได้ xx Cr. รายได้รับล่วงหน้า(หนี้สิน) xx

xx.")

24

3.Converting Liabilities to Revenue

Initially, revenues that benefit more than one accounting period are recorded as Revenue. 4

25

3.Converting Liabilities to Revenue

Over time, the Unearned revenue is decreased when the revenue is recognized as it is earned.(สมมุติว่าปิดบัญชีทุกสิ้นเดือน) 4

4.")

26

3.Converting Liabilities to Revenue

Balance Sheet Liability for future periods. Income Statement Revenue earned this period. 4

27

3.Converting Liabilities to Revenue

2.บันทึกเป็นหนี้สิน 2.1 ตอนรับเงิน: Dr. เงินสด xx Cr. รายได้รับล่วงหน้า xx 2.2 ปรับปรุงตอนสิ้นงวด: Dr. รายได้รับล่วงหน้า xx Cr. รายได้ xx

28

3.Converting Liabilities to Revenue

Initially, revenues that benefit more than one accounting period are recorded as liabilities. 4

29

3.Converting Liabilities to Revenue

Over time, the revenue is recognized as it is earned. 4

30

3.Converting Liabilities to Revenue

Balance Sheet Liability for future periods. Income Statement Revenue earned this period. 4

31

4.Converting Assets to Expenses

End of Current Period Prior Periods Current Period Future Periods Transaction Paid future expenses in advance (creates an asset). Adjusting Entry Recognizes portion of asset consumed as expense, and Reduces balance of asset account. 4

. Adjusting Entry. Recognizes portion of asset consumed as expense, and. Reduces balance of asset account. 4.")

32

4.Converting Assets to Expenses

Examples Include: Supplies Expiring Insurance Policies 4

33

4.Converting Assets to Expenses

$2,400 Insurance Policy Coverage for 12 Months $200 Monthly Insurance Expense Jan. 1 Dec. 31 On January 1, Webb Co. purchased a one-year insurance policy for $2,400. 4

34

4.Converting Assets to Expenses

ตอนจ่ายเงินสด บันทึกบัญชีได้ 2 วิธี 1.บันทึกเป็นค่าใช้จ่ายทั้งจำนวน 2.บันทึกไว้เป็นสินทรัพย์ (ค่าใช้จ่ายจ่ายล่วงหน้า) เมื่อสิ้นงวดการปรับปรุงจะแตกต่างกันระหว่าง 2 วิธี แต่ผลลัพธ์จะเท่ากัน

เมื่อสิ้นงวดการปรับปรุงจะแตกต่างกันระหว่าง 2 วิธี แต่ผลลัพธ์จะเท่ากัน.")

35

4.Converting Assets to Expens

1.บันทึกเป็นค่าใช้จ่ายทั้งจำนวน 1.1 ตอนจ่ายเงิน: Dr. ค่าใช้จ่าย xx Cr. เงินสด xx 1.2 ปรับปรุงตอนสิ้นงวด: Dr. ค่าใช้จ่ายจ่ายล่วงหน้า (สินทรัพย์) xx Cr. ค่าใช้จ่าย xx

xx. Cr. ค่าใช้จ่าย xx.")

36

4.Converting Assets to Expenses

Initially, costs that benefit more than one accounting period are recorded as Expenses. 4

37

4.Converting Assets to Expenses

Unexpired costs is recognized as asset 4

38

4.Converting Assets to Expenses

Balance Sheet Cost of assets that benefit future periods. Income Statement Cost of assets used this period to generate revenue. 4

39

4.Converting Assets to Expens

2.บันทึกเป็นสินทรัพย์ 2.1 ตอนจ่ายเงิน: Dr. ค่าใช้จ่ายจ่ายล่วงหน้า xx Cr. เงินสด xx 2.2 ปรับปรุงตอนสิ้นงวด: Dr. ค่าใช้จ่าย xx Cr. ค่าใช้จ่ายจ่ายล่วงหน้า xx

40

4.Converting Assets to Expenses

Initially, costs that benefit more than one accounting period are recorded as assets. 4

41

4.Converting Assets to Expenses

The costs are expensed as they are used to generate revenue. 4

42

4.Converting Assets to Expenses

Balance Sheet Cost of assets that benefit future periods. Income Statement Cost of assets used this period to generate revenue. 4

43

Uncollectible/Doubtful Accounts:

If a company makes credit sales to customers, some accounts inevitably will turn out to be uncollectible.

44

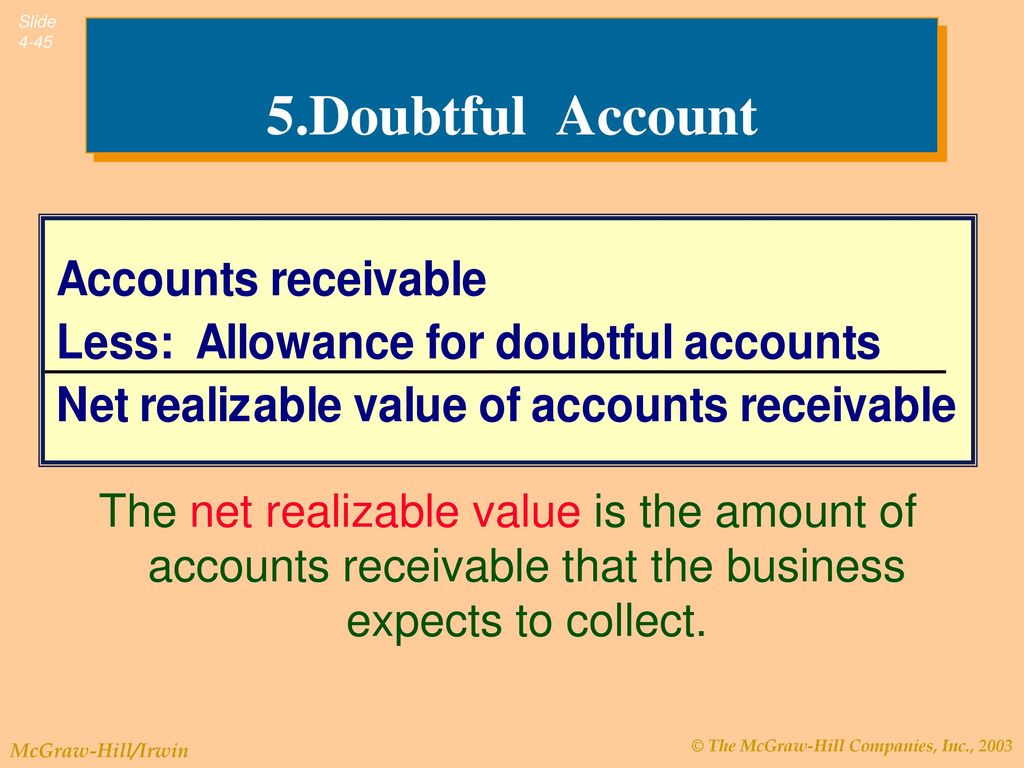

5.Doubtful Account At the end of each period, record an estimate of the uncollectible accounts. Selling expense Contra-asset account

45

5.Doubtful Account The net realizable value is the amount of accounts receivable that the business expects to collect. 49 49

46

6.The Concept of Depreciation

Depreciable assets are physical objects that retain their size and shape but lose their economic usefulness over time. Depreciation is the systematic allocation of the cost of a depreciable asset to expense.

47

6.The Concept of Depreciation

The portion of an asset’s utility that is used up must be expensed in the period used. Fixed Asset (debit) The asset’s usefulness is partially consumed during the period. Accumulated Depreciation (credit) On date when initial payment is made . . . At end of period . . . Depreciation Expense (debit) Cash (credit)

The asset’s usefulness is partially consumed during the period. Accumulated Depreciation (credit) On date when initial payment is made At end of period Depreciation Expense (debit) Cash (credit)")

48

6.Depreciation Is Only an Estimate

On May 2, 2003, JJ’s Lawn Care Service purchased a lawn mower with a useful life of 50 months for $2,500 cash. Using the straight-line method, calculate the monthly depreciation expense. Depreciation expense (per period) = Cost of the asset Estimated useful life $2,500 50 = $50

= Cost of the asset. Estimated useful life. $2, = $50.")

49

6.Depreciation Is Only an Estimate

JJ’s Lawn Care Service would make the following adjusting entry. Contra-asset 4

50

6.Depreciation Is Only an Estimate

JJ’s $15,000 truck is depreciated over 60 months as follows: $15,00060 months = $250 per month 4

51

Accumulated depreciation would appear on the balance sheet as follows:

4

52

Effects of the Adjusting Entries

Journalize transactions. Post entries to the ledger accounts. Prepare trial balance. Make end-of-year adjustments. Prepare adjusted trial balance. Recall from the accounting cycle discussed in Chapter 4, that after the adjusting entries are made, an adjusted trial balance is prepared. 3

53

This is the Adjusted Trial Balance for JJ’s.

Now, let’s prepare the financial statements for JJ’s Lawn Care Service for May. 4

54

Closing the Temporary Equity Accounts

The closing process gets the temporary accounts ready for the next accounting period. Close Revenue accounts to Income Summary. Close Expense accounts to Income Summary. Close Income Summary account to Retained Earnings. Close Dividends to Retained Earnings. 4

55

Closing Entries for Revenue Accounts

Since Sales Revenue has a credit balance, the closing entry requires a debit to the Sales Revenue account. 4

56

Closing Entries for Revenue Accounts

57

Closing Entries for Expense Accounts

Since expense accounts have a debit balance, the closing entry requires a credit to the expense accounts. 4

58

Closing Entries for Expense Accounts

Net Income

59

Closing the Income Summary Account

Since Income Summary has a $400 credit balance, the closing entry requires a debit to Income Summary. 4

60

Closing the Income Summary Account

The balance in Income Summary is now zero.

61

Closing the Dividends Account

Since the Dividends account has a debit balance, the closing entry requires a credit to the Dividends account. 4

62

Closing the Dividends Account

63

After all closing entries are made, JJ’s After-Closing Trial Balance looks like this.

4

64

Preparing Financial Statements Covering Different Periods of Time

Many companies prepare financial statements at various points throughout the year. Annually Quarterly Interim Financial Statements Monthly Jan. 1 Dec. 31 3

65

Openning Entries เมื่อเริ่มต้นงวดบัญชีใหม่ ให้บันทึกรายการเปิดบัญชีในสมุดรายวันทั่วไปเล่มใหม่ด้วยจำนวนยอดคงเหลือในรายการสินทรัพย์ หนี้สิน และส่วนของผู้เป็นเจ้าของแล้วผ่านรายการไปบัญชีแยกประเภทที่เกี่ยวข้องในสมุดบัญชีแยกประเภททั่วไปเล่มใหม่เป็นยอดคงเหลือยกมา

66

ภาคผนวกบทที่ 5 การกลับรายการ(Reversing Entries)

คือการกลับรายการปรับปรุงที่ได้บันทึกไว้เมื่อสิ้นงวดก่อน เสมือนไม่มีรายการนั้นๆเกิดขึ้น เพื่อให้การบันทึกบันชีในงวดใหม่สะดวกขึ้นเพราะไม่ต้องคำนึงถึงยอดในบัญชีที่ถูกปรับปรุงมาก่อน การกลับรายการปรับปรุงจะทำเฉพาะที่เกี่ยวกับรายได้และค่าใช้จ่าย ยกเว้นรายการปรับปรุงหนี้สงสัยจะสูญและค่าเสื่อมราคา กิจการจะกลับรายการปรับปรุงตอนต้นงวดหรือไม่ก็ได้ แต่หากไม่มีการกลับรายการปรับปรุง การบันทึกบัญชีในระหว่างงวดต้องคำนึงถึงยอดรายการที่เคยปรับปรุงมาด้วย

67

กระดาษทำการอาจมีจำนวน 8 ช่อง 10 ช่อง แล้วแต่ความต้องการ

Working Paper กระดาษทำการเป็นเครื่องมือช่วยนักบัญชีในการจัดทำงบการเงินให้รวดเร็วขึ้นและไม่ผิดพลาด กระดาษทำการอาจมีจำนวน 8 ช่อง 10 ช่อง แล้วแต่ความต้องการ

68

End of Chapter 5 4

งานนำเสนอที่คล้ายกัน

. 12-2 Understanding the Business A company may invest in the securities of another company to: Earn a return on idle funds.>")

Chapter 3.>")

Chapter 6 2.>")